This is one of a series on how to handle items that affect the "basis" of tax.

This is one of a series on how to handle items that affect the "basis" of tax.Let's say you're interested in a computer - the Univac Model 4206. If you buy it from Gene's Finer Computing Machines, he will charge you his "friend" price of $100,000 (it's a nice computer).

In today's mail, you got a letter from Univac offering you a rebate of $5,000 if you buy your 4206 before the end of the month. That works for you so you get yourself over to Gene and buy that computer. You mention that the rebate brought you in, and Gene kindly offers to handle the rebate for you if you'll sign it over to him.

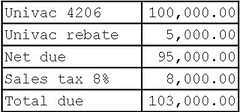

Gene sells you the computer and the invoice shows:

The basis for the tax calculation is $100,000, not 95,000. The reason is that, while it looks like you're getting a discount which ought to reduce the tax base, you're really paying $100,000. $95,000 is coming out of your pocket and $5,000 is being paid by Xerox. As far as Gene is concerned, he's still sold that copier for $100,000 and that is what he'll report as his gross sales.

Think about it this way. Maybe Gene wasn't able to cash in the rebate for you. In that case, you'd file for that rebate later. Then Gene is obviously going to have to charge you sales tax on the full $100,000.

So rebates generally do NOT reduce the tax basis because the original sale amount is still being paid. There are a few states that do reduce the tax base by rebates but you could count them on the fingers of one hand. And there are some states that handle rebates for vehicles differently. Check the local laws.

Here is a later article on a related topic - coupons.

Sales Tax Guy

See disclaimer

Here's information on our upcoming seminars and webinars And we do coaching!

And please don't forget to visit our advertisers!

No comments:

Post a Comment