He collected money but didn't pay it. Allegedly. But he didn't go to jail - probation. Man, doesn't anyone go to jail on this stuff?!?

Bristol businessman pleads guilty to tax fraud

Friday, December 15, 2006

Saturday, December 09, 2006

Where can I find certificate information?

Obviously, one resource to find information is the web site for whatever state you're interested in. BUT, if you want a single resource, I recommend the Guide to Sales and Use Taxes from RIA. They have a very useful separate section in each state chapter for state certificate requirements.

One other issue. As a good rule of thumb, the certificate should be from the state where the ultimate consumer receives the goods. So if A in Illinois ships to B in Florida and bills B's office in Nevada, A should get a Florida resale certificate.

Sales Tax Guy

see disclaimer

One other issue. As a good rule of thumb, the certificate should be from the state where the ultimate consumer receives the goods. So if A in Illinois ships to B in Florida and bills B's office in Nevada, A should get a Florida resale certificate.

Sales Tax Guy

see disclaimer

Thursday, November 30, 2006

Sentenced to Seven Years in Jail!

But the sentenced was suspended. What a gyp! Here's the article.

And in this case, a restaurant owner was indicted for allegedly not paying over $100,000 in taxes collected. What's interesting is that one of his staff now owns the business - she knew what was going on and waited until he got in over his head, then managed to snag the business from him. Sneaky. Here's the article.

We're a Non-Profit!

Big deal! So what?

Big deal! So what?I’m being rude and crude to point out that just because the IRS says you’re a non-profit organization (or not-for-profit, if you'd prefer) may mean absolutely nothing for sales tax and/or use tax purposes.

I’d estimate that close to one third of the states do not provide a broad exemption from sales and use tax for purchases made by non-profit organizations. And even if you are exempt in your state, that exemption means nothing in other states, where you might be doing a trade show, providing services, have an office, etc.

For example, let's say you're a non-profit organization in Nashville and you're registered with the state of Tennessee and have your number, certificate, etc. If you happen to be in Huntsville for a meeting and need a replacement laptop, the Huntsville OfficeMax is going to laugh at you when you try to use your Tennessee exemption in Alabama. OK, they may not laugh at you, but if they're paying attention, they're going to push the form back at you and apologize. Because that Tennessee exemption doesn't work in Alabama.

States that do provide a broad exemption often have their own criteria and don’t just default to the IRS rules. So you might be a 501(c)(3) located in Illinois, for example, but still not qualify to be exempt from SUT in Illinois.

Some states are very specific about who is exempt on their purchases. For example, Louisiana has few exemptions. But if you operate a free hospital, you can buy tax-free. However, it has to be a free hospital. If you're the average hospital in Louisiana, even a non-profit, you have to pay sales tax and/or use tax on your purchases.

Even if your purchases are exempt, states generally require non-profits to collect tax on their sales, just like regular businesses. There are exceptions for fund-raising events (often under occasional sales rules) and some admissions charges, but they vary dramatically from state to state. So if your organization sells stuff, particularly on a regular basis, you should assume you have to collect tax.

And you also have to worry about the nexus you may have in other states, just like regular businesses.

In other words, this entire topic of sales and use taxes may apply to you! Your purchases might be exempt, but your sales are likely to be taxable. It all depends on what states you operate in, and how and what you sell.

Oh, and vendors. If you sell to non-profits and have been assuming they're exempt all this time, you may be in for a rude shock when you get audited.

Sales Tax Guy

See disclaimer and research the issues thoroughly before making decisions

Here's information on our upcoming seminars and webinars.

Where can I find information on Sales and Use Tax

The information just isn’t out there on the Internet in an easy-to-find way. Every state has a web site which provides some information, but many are abysmal and others are fantastic. And you have to wade through each state’s page – none of them are organized in the same way.

In order of priority and value, here are your best resources for getting answers:

1. A lawyer, professional or consultant who specializes in SUT. This resource is also, without question, the most expensive.

2. An online subscription service from RIA or CCH (this is what the pros use). Which one you use is probably a function of what service your company already subscribes to for income taxes, etc. I'll bet you a nickle that your company does NOT subscribe to the sales tax portion, so you want to get that fixed.

3. Sales and Use Tax books (I like the ones from RIA and the ABA – these are also what the pros use)

4. State industry associations may be able to help, particularly if they are well funded and are in tricky industries, like manufacturing or construction. Give yours a call and see if they can help you.

5. State sales tax sites

One other thing to keep in mind. As you peruse the Internet, you will find reference sources. Folks, if it’s FREE, then it probably isn’t complete. This is a topic that requires a LOT of effort to keep up to date. So take information you find in a FREE resource with a big grain of salt, like this blog. ;-)

Another source of information to be wary of is information summarized and presented in table form or list form. Again, the information on this topic is complicated. Rarely does a table or list do justice to the material – it’s usually just too much to summarize like that.

In summary, the good information on this topic is going to cost you money. Other than state Web pages, there really isn’t any FREE, comprehensive, up-to-date and good resource available on the Web.

The Sales Tax Guy

http://salestaxguy.blogspot.com

See the disclaimer - this is for education only. Research these issues thoroughly before making decisions. Remember: there are details we haven't discussed, and every state is different. Here's more information

Get these articles in your inbox - subscribe at http://salestaxguy.blogspot.com

Here's information on our upcoming seminars and webinars.

http://www.salestax-usetax.com/

Picture note: the image above is hosted on Flickr. If you'd like to see more, click on the photo.

In order of priority and value, here are your best resources for getting answers:

1. A lawyer, professional or consultant who specializes in SUT. This resource is also, without question, the most expensive.

2. An online subscription service from RIA or CCH (this is what the pros use). Which one you use is probably a function of what service your company already subscribes to for income taxes, etc. I'll bet you a nickle that your company does NOT subscribe to the sales tax portion, so you want to get that fixed.

3. Sales and Use Tax books (I like the ones from RIA and the ABA – these are also what the pros use)

4. State industry associations may be able to help, particularly if they are well funded and are in tricky industries, like manufacturing or construction. Give yours a call and see if they can help you.

5. State sales tax sites

One other thing to keep in mind. As you peruse the Internet, you will find reference sources. Folks, if it’s FREE, then it probably isn’t complete. This is a topic that requires a LOT of effort to keep up to date. So take information you find in a FREE resource with a big grain of salt, like this blog. ;-)

Another source of information to be wary of is information summarized and presented in table form or list form. Again, the information on this topic is complicated. Rarely does a table or list do justice to the material – it’s usually just too much to summarize like that.

In summary, the good information on this topic is going to cost you money. Other than state Web pages, there really isn’t any FREE, comprehensive, up-to-date and good resource available on the Web.

The Sales Tax Guy

http://salestaxguy.blogspot.com

See the disclaimer - this is for education only. Research these issues thoroughly before making decisions. Remember: there are details we haven't discussed, and every state is different. Here's more information

Get these articles in your inbox - subscribe at http://salestaxguy.blogspot.com

Here's information on our upcoming seminars and webinars.

http://www.salestax-usetax.com/

Picture note: the image above is hosted on Flickr. If you'd like to see more, click on the photo.

Monday, November 27, 2006

Searching Google for Sales Tax Bad Guys

As I've mentioned in my seminars, it's fun to occasionally to a Google search on "sales tax" felony to see who's getting in serious trouble for sales tax violations.

Here's a video store owner who allegedly "misapplied" his sales tax collections.

Here's one about a guy who allegedly reported a boat purchase (and paid taxes when he registered it) with a value of $4000 vs. the real price of $40,000. And there is other stuff going on here that makes this a real soap opera. The taxes are just the beginning.

A restaurant in Michigan REALLY got in trouble for allegedly hiring illegal workers, and not remitting sales tax and employment taxes.

I'll be reporting on some of the more interesting cases every week or so from now on.

Sales Tax Guy

Sunday, November 19, 2006

The Worst Source of Information

When I rank information sources in my seminar, this one is the lowest on the list...

"We've always done it this way."

Or variation number 1:

"They told me to do it this way."

Or variation number 2:

"My predecessor told me to do it this way."

The most amazing example of this came up this week when a woman in the seminar told me their method for determining the taxability of their purchases (they've always done it this way):

If the vendor charges freight, the purchase is taxable. If the vendor didn't charge freight, then the purchase isn't taxable.

Sigh.

Sales Tax Guy

Thursday, November 16, 2006

How far can we go back for a refund?

Another question...two in one day! How exciting!: How far can we go back? We've been overpaying a vendor for many years. Is it reasonable to expect a refund for several years of overpaid taxes?

Generally, you can only go back 3 or 4 years, depending on your state's statute of limitations. And yes, almost every state expects you to get the refund from the vendor. And the vendor has to give you a refund. Expect resistance, however. Unless it's something obvious, like a resale issue, they may not understand the law and fight it.

In addition, if the amount is substantial, they may have to file for a refund with the state after giving you a refund...which means a cash flow problem. And finally, asking for a refund (or credit) will probably trigger an audit, which they don't want.

Good luck. And check with your CPA.

Sales Tax Guy

see the disclaimer

Generally, you can only go back 3 or 4 years, depending on your state's statute of limitations. And yes, almost every state expects you to get the refund from the vendor. And the vendor has to give you a refund. Expect resistance, however. Unless it's something obvious, like a resale issue, they may not understand the law and fight it.

In addition, if the amount is substantial, they may have to file for a refund with the state after giving you a refund...which means a cash flow problem. And finally, asking for a refund (or credit) will probably trigger an audit, which they don't want.

Good luck. And check with your CPA.

Sales Tax Guy

see the disclaimer

Do I have to charge tax if I've already paid tax?

Here's the question:

I have a question for the sales tax guy! I have not yet been able to find the answer. My business is registered as a self proprietership. I make jewelry. I buy my supplies from various locations, some of which charge me tax. If I pay tax on the supplies, do I still have to charge sales tax to my customer? What if I make a piece of jewelry where some I paid sales tax on some supplies, but not others?

Here's the answer:

I refer to this as the "Second Golden Rule of Sales and Use Tax."

ANYTIME there is a retail sale, tax must be charged (except for many, many exceptions). By selling your jewelry, you are making a retail sale and should be charging tax to your customers.

What you should do is buy your ingredients, the stuff that goes into your product, for RESALE. Then you don't pay tax on your purchases. You only charge tax to your customers (and remit to the state, of course).

The fact that you already paid tax doesn't get you off the hook. The object is to tax what YOU sell to the final consumer. The tax will be higher because it has your profit in it. Which is what the state wants.

So register with the state, get your resale number, use it to buy your ingredients for resale and charge your customers tax.

By the way, the other stuff you buy that doesn't go into your product, IS taxable. In that case, YOU'RE the end user. However, there might be manufacturing exceptions here, depending on the state your're in.

Thanks for the excellent question. I'd strongly suggest you talk to your CPA about this as well.

Sales Tax Guy

See disclaimer

I have a question for the sales tax guy! I have not yet been able to find the answer. My business is registered as a self proprietership. I make jewelry. I buy my supplies from various locations, some of which charge me tax. If I pay tax on the supplies, do I still have to charge sales tax to my customer? What if I make a piece of jewelry where some I paid sales tax on some supplies, but not others?

Here's the answer:

I refer to this as the "Second Golden Rule of Sales and Use Tax."

ANYTIME there is a retail sale, tax must be charged (except for many, many exceptions). By selling your jewelry, you are making a retail sale and should be charging tax to your customers.

What you should do is buy your ingredients, the stuff that goes into your product, for RESALE. Then you don't pay tax on your purchases. You only charge tax to your customers (and remit to the state, of course).

The fact that you already paid tax doesn't get you off the hook. The object is to tax what YOU sell to the final consumer. The tax will be higher because it has your profit in it. Which is what the state wants.

So register with the state, get your resale number, use it to buy your ingredients for resale and charge your customers tax.

By the way, the other stuff you buy that doesn't go into your product, IS taxable. In that case, YOU'RE the end user. However, there might be manufacturing exceptions here, depending on the state your're in.

Thanks for the excellent question. I'd strongly suggest you talk to your CPA about this as well.

Sales Tax Guy

See disclaimer

Sunday, November 05, 2006

Are Pumpkins Food?

I was getting ready to do a seminar series in Illinois and noticed this clarification issued last year by the IDOR. In Illinois, food for human consumption is taxable at a lower rate (1% state tax but some local jurisdictions can add to that). The question evidently came up as to the taxability of pumpkins.

Ready?

If it's sold whole and in edible condition, it's food. But if it's carved out, it's not food and therefore taxable at the full rate just like TPP.

Hope that clears everything up. And beware, this rule might be transferable to other states too.

This post really was just an excuse to use a picture of a pumpkin (that is clearly not used as food, but was BOUGHT as food. Therefore, we only paid the lower rate. Take THAT, IDOR!)

Sales Tax Guy

Thursday, October 05, 2006

Getting Refund of Taxes from the Vendor

Tying in with the item from a couple of days ago, what do you do if the vendor has incorrectly charged you tax, and you discover it after you've paid. You want your money back, I presume.

The best way to avoid this problem is to have good AP procedures in place to avoid improper payment of taxes. But let's assume that you don't.

One easy way to get your money back is to simply take it as a deduction or debit memo on your next payment to the vendor. This works if you still owe them money. But then you're going to have problems with the vendor who now wants HIS money back. Depending on how interested you are in keeping this vendor happy, will affect whether or not this is an operative technique.

OR you can ask for your money back (a refund). This will require you to demonstrate to the vendor how they incorrectly collected taxes from you. This conversation will have to go higher than whomever you normally talk to in the billing or receivables department. Unless it's really a mechnical problem, this issue is way beyond them. You're going to have to talk, probably, to the vendor's controller, CFO, possibly even their lawyer.

There are two problems with getting the vendor to cough up the money.

Firstly, they don't believe you. All they know about sales and use tax is what they've been told. So you're gonna have to 'splain it to them. See above.

Secondly, they don't want to give you the money back because then they have to get the money back from the state. That presents a cash flow problem for them because they usually can't get a refund from the state UNLESS they have ALREADY refunded it to the customer. And then the state is likely to audit them. Most states see a substantial request for credit or refund as an invitation to an audit. And since nobody likes being audited, the vendor has got even more reason to be reluctant to refund the money to you.

So what do you do?

Most states take the position, either officially or informally, that the only person they'll refund overpaid taxes to is the person that wrote them the check in the first place, which means the vendor. So you're stuck. You need to get the vendor to cooperate. But what if, as mentioned above, the vendor resists?

If the vendor won't cooperate, then advise the vendor that you will go directly to the state for the refund. I'd suggest you state this formally, in writing, possibly on your lawyer's letterhead. Some states WILL refund your money if the vendor won't cooperate, goes out of business, is bankrupt, etc. But it's tough. And even if the state won't refund the money to you, the threat of going to the state (and thereby opening up the vendor to the aforementioned audit) may break up the logjam.

This, by the way, is a pretty relationship-destroying approach. And may even subject YOU to an audit. I'd suggest talking to everyone concerned before using this strategy.

(Sigh) Sounds like a pretty rotten situation. Yep, it is. The best way to solve this problem is, as mentioned at the top of this article, to develop procedures to that catch overpayments before they go out the door. We've talked about some of these already on this blog, and we'll talk about more in the future. Stay tuned.

Sales Tax Guy

And, of course, note the disclaimer

The best way to avoid this problem is to have good AP procedures in place to avoid improper payment of taxes. But let's assume that you don't.

One easy way to get your money back is to simply take it as a deduction or debit memo on your next payment to the vendor. This works if you still owe them money. But then you're going to have problems with the vendor who now wants HIS money back. Depending on how interested you are in keeping this vendor happy, will affect whether or not this is an operative technique.

OR you can ask for your money back (a refund). This will require you to demonstrate to the vendor how they incorrectly collected taxes from you. This conversation will have to go higher than whomever you normally talk to in the billing or receivables department. Unless it's really a mechnical problem, this issue is way beyond them. You're going to have to talk, probably, to the vendor's controller, CFO, possibly even their lawyer.

There are two problems with getting the vendor to cough up the money.

Firstly, they don't believe you. All they know about sales and use tax is what they've been told. So you're gonna have to 'splain it to them. See above.

Secondly, they don't want to give you the money back because then they have to get the money back from the state. That presents a cash flow problem for them because they usually can't get a refund from the state UNLESS they have ALREADY refunded it to the customer. And then the state is likely to audit them. Most states see a substantial request for credit or refund as an invitation to an audit. And since nobody likes being audited, the vendor has got even more reason to be reluctant to refund the money to you.

So what do you do?

Most states take the position, either officially or informally, that the only person they'll refund overpaid taxes to is the person that wrote them the check in the first place, which means the vendor. So you're stuck. You need to get the vendor to cooperate. But what if, as mentioned above, the vendor resists?

If the vendor won't cooperate, then advise the vendor that you will go directly to the state for the refund. I'd suggest you state this formally, in writing, possibly on your lawyer's letterhead. Some states WILL refund your money if the vendor won't cooperate, goes out of business, is bankrupt, etc. But it's tough. And even if the state won't refund the money to you, the threat of going to the state (and thereby opening up the vendor to the aforementioned audit) may break up the logjam.

This, by the way, is a pretty relationship-destroying approach. And may even subject YOU to an audit. I'd suggest talking to everyone concerned before using this strategy.

(Sigh) Sounds like a pretty rotten situation. Yep, it is. The best way to solve this problem is, as mentioned at the top of this article, to develop procedures to that catch overpayments before they go out the door. We've talked about some of these already on this blog, and we'll talk about more in the future. Stay tuned.

Sales Tax Guy

And, of course, note the disclaimer

Tuesday, October 03, 2006

Vendor didn't charge tax - What do we do?

"A vendor didn't charge us the correct tax. He billed us 6%, the correct tax should have been 6.5% We advised him of this, then paid the uncharged tax as use tax on our return. A month later, he bills us for the difference. Do we owe him since we paid the tax on our own?"

Theoretically, you don't owe the sales tax since you've paid the use tax. But you messed things up by not giving the vendor a chance to do it correctly. You should have given the vendor a chance to bill you properly before you self-assessed. In the future, wait a month or two to see what the vendor does. At this point, my recommendation would be to make an worksheet adjustment to your use tax liability on your next return to get the money back from the state, and pay the vendor. That way his records are correct, and you'll avoid a long drawn out discussion with the vendor.

This may not be technically legal, but leave a good audit trail. If the auditor can understand what you've done, you should be OK. The state got their money...that's the important thing.

Sales Tax Guy

See the disclaimer

Theoretically, you don't owe the sales tax since you've paid the use tax. But you messed things up by not giving the vendor a chance to do it correctly. You should have given the vendor a chance to bill you properly before you self-assessed. In the future, wait a month or two to see what the vendor does. At this point, my recommendation would be to make an worksheet adjustment to your use tax liability on your next return to get the money back from the state, and pay the vendor. That way his records are correct, and you'll avoid a long drawn out discussion with the vendor.

This may not be technically legal, but leave a good audit trail. If the auditor can understand what you've done, you should be OK. The state got their money...that's the important thing.

Sales Tax Guy

See the disclaimer

Friday, September 29, 2006

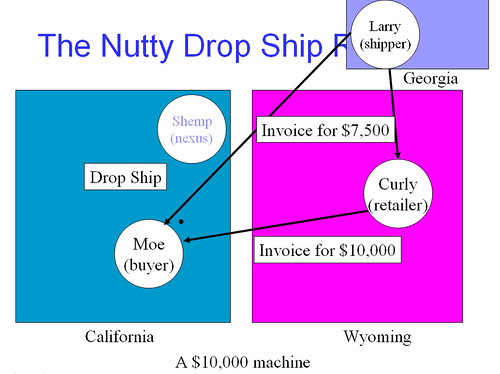

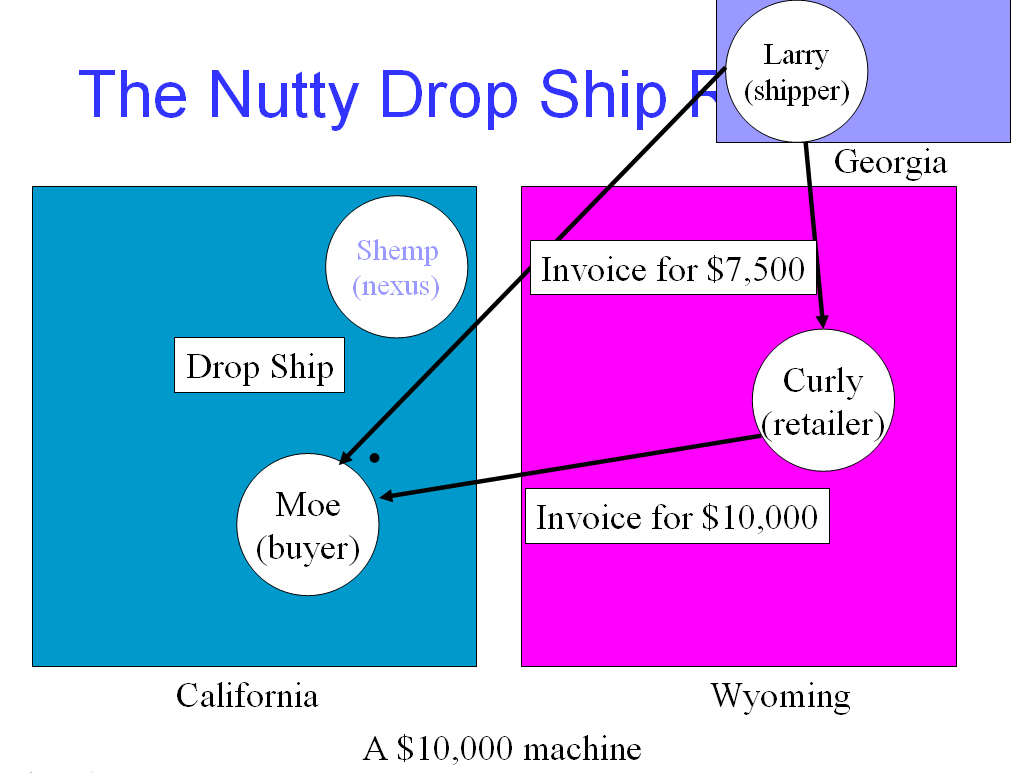

Why is my vendor charging me tax on drop shipments?

- Moe (in California) orders goods from Curly, the retailer.

- Curly (in Wyoming) orders goods from Larry, the manufacturer or distributor.

- Larry (in Georgia, but with nexus in California) ships the goods to Moe.

- Larry bills Curly.

- Curly marks it up and bills Moe.

- Curly is registered ONLY in Wyoming, has a WY resale certificate and does NOT have nexus in California. Which means he doesn’t charge Moe any tax.

In, what I like to call, the “nutty” drop ship states (California is one of them), they require that Larry must charge CA tax to Curly, even though Curly is buying for resale. They will let Larry off the hook for the tax if Curly provides Larry with a California resale certificate (and CA registration number, of course). Curly doesn’t have this because he doesn’t have nexus in CA. And he doesn’t want to register in CA and therefore collect tax because he’ll loose any competitive advantage he has in CA, aside from the other problems with letting CA know he’s out there.

So Larry must collect the tax from Curly and Curly obviously has his margins squeezed. And he can’t pass on the tax to Moe because he’s not registered to collect tax in CA.

Moe also loses here because, since he has an invoice from Curly with no tax shown, the auditor will assess him for use tax on the purchase that Larry has already paid the tax on!

Many vendors (Larry) have been caught on this issue by NDSS (nutty drop ship states), so many of them just automatically follow these rules, regardless of whether they’re shipping to a NDSS or not. This causes problems for the Curlys of the world because they’re being forced to pay tax that isn’t truly due.

If you find yourself in this situation, I recommend that you research the NDSS situation in the ship-to state, and then challenge the vendor. Make them show you where they’re required to charge tax and show them what you’ve come up with. And of course, depending on the relationship you have with the vendor, don’t pay the tax.

There's more on this here

Of course, the usual disclaimers

| Picture note: the illustration above is hosted on Flickr. If you'd like to see a larger version, click here |

{kind=link}

.tdropships

Thursday, September 28, 2006

What about Canada???

What about Canada? Yours truly knows about US sales and use tax - I don't want to even think about Canada, or (deep inhale) Mexico. Yet I get questions frequently on these two countries. So here's some advice:

1. Do a search on the following terms (or some variation that you like) :

canada

vat

sales tax

seminar

training

I did that and several items popped up that looked promising.

2. If you have a relationship with a large CPA firm (or law firm) like E & Y or Deloitte, check with them. They probably offer seminars that may be helpful. I know this because, when I did the above search, their names popped up.

So give it a try!

Sales Tax Guy

PS, you may have noticed a picture. Since I'm into photography, I thought I'd start making this blog more interesting by throwing a picture from my Flickr collection into the post that's relevent to the topic. That one is from the Columbia Ice Fields in Alberta. Click on the picture to see a bigger version of it on Flickr.

1. Do a search on the following terms (or some variation that you like) :

canada

vat

sales tax

seminar

training

I did that and several items popped up that looked promising.

2. If you have a relationship with a large CPA firm (or law firm) like E & Y or Deloitte, check with them. They probably offer seminars that may be helpful. I know this because, when I did the above search, their names popped up.

So give it a try!

Sales Tax Guy

PS, you may have noticed a picture. Since I'm into photography, I thought I'd start making this blog more interesting by throwing a picture from my Flickr collection into the post that's relevent to the topic. That one is from the Columbia Ice Fields in Alberta. Click on the picture to see a bigger version of it on Flickr.

Tuesday, September 19, 2006

MN Computer Contracts

Greetings all - told ya I'd give you an update...

Here's the MN bulletin on this topic

http://www.taxes.state.mn.us/taxes/sales/publications/revenue_notices/content/93-17.shtml

Combined support and upgrade contracts are taxable at 20% of the total.

Jim

Here's the MN bulletin on this topic

http://www.taxes.state.mn.us/taxes/sales/publications/revenue_notices/content/93-17.shtml

Combined support and upgrade contracts are taxable at 20% of the total.

Jim

Thursday, August 17, 2006

For Seminar Participants - New Handouts Available

If you've been waiting for the latest version of the handouts to be posted, they're now available at the URL you were given in the seminar.

Jim

Jim

NC Manufacturers - A Clarification

For those of you in the seminar this week from NC, manufacturers DO get an exemption from the tax. They don't have tax collected from their purchases, and they don't have to remit use tax. BUT there IS that derned privilege tax.

Jim

Jim

Thursday, August 03, 2006

More on leasing with an operator

Here are a couple of more points to consider, which are VERY objective and may help with determining this transaction's taxability:

1. Was the equipment bought by the lessor for resale?

2. Is the lease payment based on how long the equipment is leased for as opposed to the successful completion of a job?

Sales Tax Guy

1. Was the equipment bought by the lessor for resale?

2. Is the lease payment based on how long the equipment is leased for as opposed to the successful completion of a job?

Sales Tax Guy

Thursday, July 20, 2006

Leasing TPP with an operator

With the help of some folks in a recent seminar, I think I've hit on a useful "rule of thumb" for dealing with the question of leasing equipment with an operator.

In most states, leasing of TPP is taxable. But the question is, if I get an operator for the equipment, two different taxation situations arise:

1. Am I still leasing a piece of equipment? If so, it's taxable (in most states); or

2. Am I hiring the services of an operator (which may or may not be taxable) and the equipment is just incidental to her service.

The problem is knowing when you've gone from situation1 to situation 2.

Here's the rule of thumb:

When the operator ONLY has control over the actual operation of the machine (pushing buttons, pulling levers, etc.) and has NO control over what is actually done with the equipment, then you're in situation 1; you're still leasing a piece of equipment and it's taxable (in most states).

When the operator not only has control over the operation of the machine, but decides how and where to use it, then you're probably hiring the services of the operator, and then you look at whether her services are taxable.

To summarize, if their control is limited to the console or cab of the machine, you're still leasing a machine. But if their control extends outside of the cab to the actual use of the machine, then you're probably hiring the services of the operator and the machine is something THEY use to perform that service. Then the question is: is that service taxable?

Of course, the specific rules in every state will be different.

Clear? Yeah, right.

Sales Tax Guy

The usual disclaimers apply

Wednesday, June 21, 2006

Golden Rule - Which state has jurisdiction over the sale

The state that has jurisdiction over an interstate sale will be the state where delivery occurs.

This is usually where physical control or the right of control transfers from the seller to the buyer. Since, in an interstate sale, the only thing that can be taxed is the buyer's use of the TPP, and since use involves control over the TPP, then the delivery point determines, for all practical purposes, the state that gets to impose the use tax.

In other words, where is the delivery point?

Another way to look at it is where the seller completes their duties. This is particularly helpful when you're dealing with a situation involving a long installation.

A few (and I do mean a few) states use FOB points to determine the state that has jurisdiction. That can be overcome by the buyer negotiating FOB destination.

Use of this Golden Rule will help you resolve complex transactions to the specific state whose rules need to be followed.

There's a corollary to this rule

There's a little mini-course on this rule.

The Sales Tax Guy

This is usually where physical control or the right of control transfers from the seller to the buyer. Since, in an interstate sale, the only thing that can be taxed is the buyer's use of the TPP, and since use involves control over the TPP, then the delivery point determines, for all practical purposes, the state that gets to impose the use tax.

In other words, where is the delivery point?

Another way to look at it is where the seller completes their duties. This is particularly helpful when you're dealing with a situation involving a long installation.

A few (and I do mean a few) states use FOB points to determine the state that has jurisdiction. That can be overcome by the buyer negotiating FOB destination.

Use of this Golden Rule will help you resolve complex transactions to the specific state whose rules need to be followed.

There's a corollary to this rule

There's a little mini-course on this rule.

The Sales Tax Guy

Saturday, May 27, 2006

Certificates

Here are some thoughts about accepting certificates (exemption and resale) from your customers:

1. GET THEM! Get them before you ship to avoid hassles down the road, and to assure that the sale IS exempt, and the sales rep isn't trying to slip something past you.

2. Make sure they are completely filled out, per the form's instructions.

3. Check the rules for the state where the delivery is made. If it's a "drop ship rule" state, you'll need the resale certificate (and registration number) from that state.

4. As a general rule, getting the certificate from the state where the final delivery is made is a good idea.

5. Make sure the registration number is from the correct state. Watch out for FEIN numbers, which are often used incorrectly.

6. Accept the certificates in "good faith." If there's something about the transaction that you know is not exempt, either because the certificate itself is obviously a problem, or you just know that what you're selling isn't exempt, then you should charge tax. You're not accepting it in good faith.

7. In certain situations, states put an added burden beyond good faith. To be safe, ask your customer to also provide you with a copy of whatever paperwork they got from the state (eg. the resellers permit). For even more protection, confirm the number is valid with the state. Some allow an automated process, confirmation by email, or may provide a look-up function on their web site.

8. Check expiration dates for the various states. You're probably in good shape if you refresh your certificates every three years. Simply go through your customer list and ask for a new certificate from one third of them every year. That way, you'll never have a certificate that's more than three years old.

9. Speaking of dates, make sure that the dates match your sale. It won't do you any good to get an exemption certificate that's effective in 2006 if your sales to the customer were in 2005.

10. There is software available to help you manage this process. I won't make any recommendations, but a web search may help you.

11. Follow the instructions, both on the form and on the state's web site when accepting certificates.

Sales Tax Guy

See disclaimer

1. GET THEM! Get them before you ship to avoid hassles down the road, and to assure that the sale IS exempt, and the sales rep isn't trying to slip something past you.

2. Make sure they are completely filled out, per the form's instructions.

3. Check the rules for the state where the delivery is made. If it's a "drop ship rule" state, you'll need the resale certificate (and registration number) from that state.

4. As a general rule, getting the certificate from the state where the final delivery is made is a good idea.

5. Make sure the registration number is from the correct state. Watch out for FEIN numbers, which are often used incorrectly.

6. Accept the certificates in "good faith." If there's something about the transaction that you know is not exempt, either because the certificate itself is obviously a problem, or you just know that what you're selling isn't exempt, then you should charge tax. You're not accepting it in good faith.

7. In certain situations, states put an added burden beyond good faith. To be safe, ask your customer to also provide you with a copy of whatever paperwork they got from the state (eg. the resellers permit). For even more protection, confirm the number is valid with the state. Some allow an automated process, confirmation by email, or may provide a look-up function on their web site.

8. Check expiration dates for the various states. You're probably in good shape if you refresh your certificates every three years. Simply go through your customer list and ask for a new certificate from one third of them every year. That way, you'll never have a certificate that's more than three years old.

9. Speaking of dates, make sure that the dates match your sale. It won't do you any good to get an exemption certificate that's effective in 2006 if your sales to the customer were in 2005.

10. There is software available to help you manage this process. I won't make any recommendations, but a web search may help you.

11. Follow the instructions, both on the form and on the state's web site when accepting certificates.

Sales Tax Guy

See disclaimer

Sunday, April 09, 2006

States doing more to find you

In the April 17th issue of BusinessWeek (page 34), there's an article on how the states and IRS are using data-mining techniques to find you. In non-technical terms, the states are reviewing other databases and records to look for something fishy.

Texas, for example, has collected $5 million dollars in the last 6 months by comparing federal airplane registrations with state tax records to find companies that haven't paid their use tax on the planes. Bad, bad companies.

In the past, states didn't have the expertise, staff or equipment to do some of these projects. But now things are getting cheaper, easier and they're outsourcing.

Another interesting scenario was a typical pizza parlor. The state might compare the sales tax returns with the personal returns of the owner with the returns filed by other pizza shops in the area with sales by vendors TO that pizza shop.

It's getting tougher and tougher to fly under the radar.

Here are the states the article mentioned: Texas, Iowa, Virginia and Massachusetts. But beware, your state may read BusinessWeek too!

Texas, for example, has collected $5 million dollars in the last 6 months by comparing federal airplane registrations with state tax records to find companies that haven't paid their use tax on the planes. Bad, bad companies.

In the past, states didn't have the expertise, staff or equipment to do some of these projects. But now things are getting cheaper, easier and they're outsourcing.

Another interesting scenario was a typical pizza parlor. The state might compare the sales tax returns with the personal returns of the owner with the returns filed by other pizza shops in the area with sales by vendors TO that pizza shop.

It's getting tougher and tougher to fly under the radar.

Here are the states the article mentioned: Texas, Iowa, Virginia and Massachusetts. But beware, your state may read BusinessWeek too!

Monday, March 13, 2006

Hey, Texans!

As promised, the latest version of the presentation has been uploaded at the location I gave you. In addition, several people have asked about local taxing issues and I promised a link to the publication on the state's web site. Here it is.

All of my Texas links are here.

Jim

All of my Texas links are here.

Jim

Friday, March 03, 2006

Contractors charging tax?

In most states, contractors pay tax on their purchases and don't charge their contracting customers tax. The problem arises for contractors that have a retail side of their business too.

If most of what they buy is for resale, but they do some contracting too, then they'll generally buy for resale and self-assess use tax on whatever they consume for the contracting business.

But if they buy mostly for the the contracting business (their use), but sell some as well, then they should probably pay tax on all of their purchases. But they've already paid tax! Therein lies the problem. What I'll recommend is specifically sanctioned by some states, and makes logical sense everywhere else. When you sell something (and charge tax) on something you have already paid tax on, then simply adjust your use tax basis on your return for the amount that you sold. That should square everything up.

Is is legal? As I said, in many states yes. In other states, they're usually silent on the issue. It certainly is a defenseable (and logical approach to take). Just don't tell em I said so. ;-)

Sales Tax Guy

See disclaimer

If most of what they buy is for resale, but they do some contracting too, then they'll generally buy for resale and self-assess use tax on whatever they consume for the contracting business.

But if they buy mostly for the the contracting business (their use), but sell some as well, then they should probably pay tax on all of their purchases. But they've already paid tax! Therein lies the problem. What I'll recommend is specifically sanctioned by some states, and makes logical sense everywhere else. When you sell something (and charge tax) on something you have already paid tax on, then simply adjust your use tax basis on your return for the amount that you sold. That should square everything up.

Is is legal? As I said, in many states yes. In other states, they're usually silent on the issue. It certainly is a defenseable (and logical approach to take). Just don't tell em I said so. ;-)

Sales Tax Guy

See disclaimer

Tuesday, February 28, 2006

FAQ: Is postage taxable?

One of the questions I've gotten a couple of times in recent days is whether or not "postage" is taxable. I think people are getting hung up on the fact that "postage" seems protected somehow. But think of it this way. It's just a delivery charge. So the real question is whether or not delivery charges are taxable in your state.

I had a question today from a seminar participant who was being charged tax on 1099's that a printer was mailing to her vendors. He was charging tax on the postage. In her state, delivery charges are taxable. And this postage was essentially the delivery charge for shipping product produced by the vendor to the customer's accounts.

Logically, this sounds like it's taxable to me.

Remember, the issues are:

NOT that it's postage.

ARE delivery charges by the vendor taxable in the state at issue?

Sales Tax Guy

See disclaimer

I had a question today from a seminar participant who was being charged tax on 1099's that a printer was mailing to her vendors. He was charging tax on the postage. In her state, delivery charges are taxable. And this postage was essentially the delivery charge for shipping product produced by the vendor to the customer's accounts.

Logically, this sounds like it's taxable to me.

Remember, the issues are:

NOT that it's postage.

ARE delivery charges by the vendor taxable in the state at issue?

Sales Tax Guy

See disclaimer

Tuesday, February 14, 2006

Why not let my customer pay the use tax?

If my customer pays the use tax, why do I have to charge him tax. Can't I get a letter from him that says he'll take care of it?

The answer is, generally, NO! The state doesn't trust your customer (and with good reason, I might add) to pay the use taxes. You're the seller and you are primarily responsible to collect the sales (or use) taxes from the customers. Even if they "promise" they'll pay.

Most states have a "direct pay permit" which DOES get you off the hook. This is a state-sanctioned way for a customer to tell you, "we'll take care of the use tax ourselves." The customer has to apply for the permit, and they will generally go through more audits than the rest of us. That's because the state really DOESN'T TRUST anyone to pay their use taxes.

Bottom line, you have to collect the taxes from your customer.

Sales Tax Guy

The answer is, generally, NO! The state doesn't trust your customer (and with good reason, I might add) to pay the use taxes. You're the seller and you are primarily responsible to collect the sales (or use) taxes from the customers. Even if they "promise" they'll pay.

Most states have a "direct pay permit" which DOES get you off the hook. This is a state-sanctioned way for a customer to tell you, "we'll take care of the use tax ourselves." The customer has to apply for the permit, and they will generally go through more audits than the rest of us. That's because the state really DOESN'T TRUST anyone to pay their use taxes.

Bottom line, you have to collect the taxes from your customer.

Sales Tax Guy

Wednesday, January 04, 2006

Direct Pay Certificates

First of all, what is a "Direct Pay Certificate?" In most states, larger organizations find them helpful because these types of companies buy lots of different things, some exempt and some taxable. This is particularly true for manufacturers, contractors and utilities. It's easier for them to get a direct pay certificate from the state. This allows them to buy pretty much everything without the vendor having to charge sales tax. The direct pay permit holder then self-assesses the use tax. Now you may think this is a pretty good idea. But there are catches:

1. States don't like to hand DP certificates out like Skittles. Don't think of this as a way of avoiding/evading tax or getting to hold onto the tax money a little longer. Generally states only give these out to larger companies with a need.

2. You can pretty much count on getting audited every three years. Because the state is now relying on your company 100% to self-assess (and we know how reliable most of us are at doing that), the state is going to be much more likely to audit you. Regularly. Frequently. Set up an office just for the auditors, if you know what I mean.

3. Tied in with number 2, you're likely to get audited before they even give you the permit, just to see if you have the systems in place to self-assess properly.

4. Finally, beware of mixing up which vendors you pay sales tax and which ones you don't (by giving them the DP certicate). I've talked with taxpayers who were not consistent in using their DP certificate. This resulted in paying sales tax on purchases and then turning around and self-assessing tax on the same purchase. At lease keep very close track of who you give a DP certicate to and who you don't.

Sales Tax Guy

1. States don't like to hand DP certificates out like Skittles. Don't think of this as a way of avoiding/evading tax or getting to hold onto the tax money a little longer. Generally states only give these out to larger companies with a need.

2. You can pretty much count on getting audited every three years. Because the state is now relying on your company 100% to self-assess (and we know how reliable most of us are at doing that), the state is going to be much more likely to audit you. Regularly. Frequently. Set up an office just for the auditors, if you know what I mean.

3. Tied in with number 2, you're likely to get audited before they even give you the permit, just to see if you have the systems in place to self-assess properly.

4. Finally, beware of mixing up which vendors you pay sales tax and which ones you don't (by giving them the DP certicate). I've talked with taxpayers who were not consistent in using their DP certificate. This resulted in paying sales tax on purchases and then turning around and self-assessing tax on the same purchase. At lease keep very close track of who you give a DP certicate to and who you don't.

Sales Tax Guy

Subscribe to:

Posts (Atom)