A reader today posed this scenario.

There is an obvious question hereMark is the manufacturer and sells to the retailerRhonda is the retailer who sells to the customerCalvin is the customerApparently, Mark is charging Rhonda sales tax.Rhonda therefore incurs the cost of the sales tax.Rhonda would like to pass on this cost to her customer, Calvin.Can she?

Why can't Rhonda buy from Mark for resale? This would seem to be the obvious and legal solution. Particularly since Rhonda is required to charge Calvin tax if the sale is taxable and she has nexus in the state.

Two exceptions spring to mind

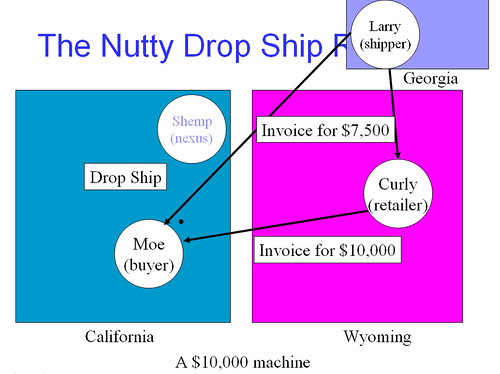

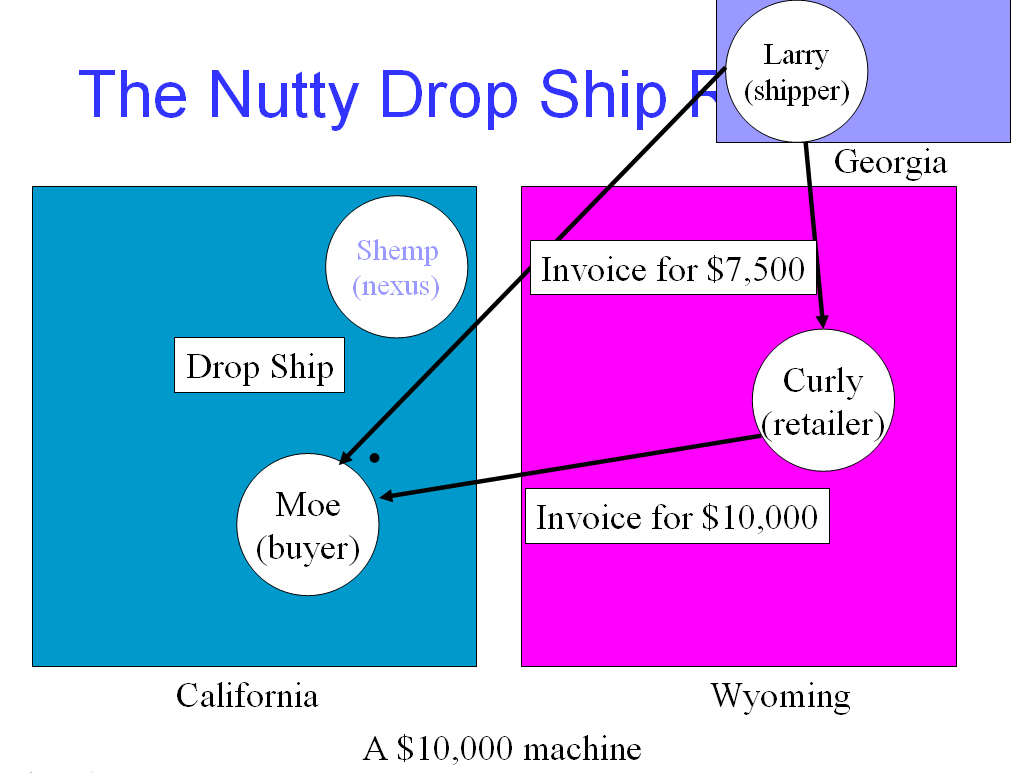

It's possible that this is a drop shipment and Mark has to charge Rhonda tax but Rhonda doesn't have a way to charge Calvin tax since she has no nexus in the delivery state.

It's also possible that Rhonda is a contractor. In most states, she pays tax to her vendors for her building materials but doesn't charge tax when she bills Calvin for the job.

These are the obvious and common exceptions - there are more.Other than the above exceptions, Rhonda should be buying for resale and charging tax, if the sale is taxable.

However, if she is incurring sales tax for some reason (like the two listed above) and she can't pass it on, or is not allowed to pass it on, then it's a cost of doing business, and she has the ability to fold the tax into the price of her goods. The only obvious restrictions I can see are:

Rhonda doesn't price herself out of the market and

the customer agrees to the priceNote that these are not sales tax law restrictions...this is just business. Rhonda can set her price at any point she wishes, as long as the customer agrees.

However...

Rhonda generally can't charge Calvin something called "tax" in a state where she isn't registered. Rhonda might think this is a way to recover the money from the customer without having to negotiate a new price. Unfortunately the law generally requires that you must be registered in a state before you charge that state's taxes. In addition, if she were to be audited, the state would ask her why she has not remitted that "tax" money to the state. If Rhonda needs to show a charge on the invoice, call it a "we're going to hold you upside down and shake money out of your pockets" surcharge. But don't put the word "tax" on Rhonda's invoice to Calvin.

And if Rhonda is making a taxable sale to Calvin, then she is required to charge Calvin tax, if she has nexus in the state. And she should obviously be buying for resale.

Bottom line

If Rhonda is making a sale to Calvin that is taxable and she has nexus in the state, she should be charging Calvin tax.

If the vendor is charging her tax, she should figure out why she can't buy it for resale.

If it's some other situation where she's incurring tax as a cost, she can't pass it on as "tax." But she can fold that cost, like any other cost, into her price.

Geez, this stuff is complicated! If you're reading this and desperately waving your hand because Jim missed something, I know. But the more holes I fill in, the less understandable this is. Suffice to say, it's messy.

And don't even get me started on absorption

The Sales Tax Guy http://salestaxguy.blogspot.com

See the disclaimer on the right.

Don't forget our upcoming seminars and webinars. http://www.salestax-usetax.com and there's more sales tax news and links here http://salestaxnews.blogspot.com

Picture note: the image above is hosted on Flickr. If you'd like to see more, click on the photo.

{kind=link}