Imagine my surprise when I saw that my favorite topic (well almost my favorite topic), made the Drudge Report. Here's the direct link. Apparently Rhode Island is getting a little nasty with sales tax enforcement.

Sales Tax Guy

Thursday, July 30, 2009

Wednesday, July 29, 2009

FAQ: International Shipments

If you ship out of a state, it really doesn't matter if you're shipping from Missouri across the Mississippi River to Illinois or a little further to Australia. The fact remains that you've shipped out of Missouri. Therefore, based on this golden rule and this golden rule, Missouri tax doesn't apply. You might have to worry about Australia taxes, but that's not my problem.

If you ship out of a state, it really doesn't matter if you're shipping from Missouri across the Mississippi River to Illinois or a little further to Australia. The fact remains that you've shipped out of Missouri. Therefore, based on this golden rule and this golden rule, Missouri tax doesn't apply. You might have to worry about Australia taxes, but that's not my problem.Conversely, if you're in Australia and you ship to Missouri, and if you have nexus in Missouri, the Missouri taxes will apply, even if you're a loonnggg way away in the land down-under.

Sales Tax Guy

| See disclaimer |

| Here's information on our upcoming seminars and webinars |

And please don't forget to visit our advertisers! |

| Picture note: the picture above is from St. Louis Missouri and is hosted on Flickr. If you'd like to see a larger version, click here, then click on the "all sizes" button above the picture. I've never been to Australia, so... |

Tuesday, July 28, 2009

The Four Loopholes (Loophole Number 2)

There are four loopholes which created the need for use tax. Over a short period of time after inventing sales tax, the states started discovering that there were some situations where they weren't able to get the sales tax revenue they were expecting. We'll use this series of posts to discuss each one.

There are four loopholes which created the need for use tax. Over a short period of time after inventing sales tax, the states started discovering that there were some situations where they weren't able to get the sales tax revenue they were expecting. We'll use this series of posts to discuss each one.The Vendor Makes a Mistake

The vendor (Steve) sells Mike a machine and, for whatever reason, fails to charge Mike sales tax. What will happen to Mike when he gets audited and the eagle-eyed auditor notices that there is no tax on the invoice? Hmm?

[I'm trying to recreate a seminar experience here, folks. So I need someone to blurt out the answer. ]

[Waiting....]

Yes, absolutely correct. Gold star for Mary! The auditor will make Mike (the buyer) pay the use tax. In most states (but not all) the buyer, for all intents and purposes, has the burden of the sales tax imposed on him. If it is not, the buyer will have to pay the use tax. But the buyer's burden is usually relieved by simply having a receipt from the seller showing that sales tax was charged.

{kind=link}

Since Steve (the seller) didn't charge Mike tax and therefore Mike has no tax receipt, Mike will get burned at audit time. Or, if Mike has a good AP specialist, he (or she) may have spotted Steve's mistake and accrued the tax in the meantime. Either way, the state gets their money. They either get it from Steve (the vendor) when he does his job correctly. Or they get it from Mike (the buyer) later.

The loophole was that if the seller didn't charge tax, the state couldn't get the money from anyone but the seller. But when they invented use tax, they had a mechanism to get the tax from the buyer as well. Nifty.

Here's a question though. Did Steve screw up? What if he absorbed the tax? Or what if he knows the item isn't taxable? If the AP specialist, or the auditor, simply reacts to the invoice not having tax, then Mike might over pay his use tax. Heavens!

That's another article.

Sales Tax Guy

| See disclaimer |

| Here's information on our upcoming seminars and webinars |

| And please don't forget to visit our advertisers! |

Picture note: I wanted a picture the shows a mistake clearly being made by someone.

Friday, July 24, 2009

We're a foreign company....

I got a version of this question this week:

"We're a non-US company who has, up until now, avoided a physical presence in the US. We ship products to US customers (usually distributors and dealers) but have no reps, warehouses, plants, offices, etc. anywhere in the States. We're considering establishing warehouses in a few places and figure that will give us nexus in those states. Where do we find advice on making this decision that isn't going to be expensive?"

That last question makes this question pretty much applicable to all of you...

There really isn't a cheap solution. The best (and most expensive) one is to hire one of the giant CPA firms and have them do a study for you. It would take into consideration sales and use tax rates, complexity, audit friendliness, rules about nexus, certificate requirements, drop shipping, any possible and unusual exemptions you might be able to take, etc.

For example, there's at least one state that has an exemption for warehousing equipment, conveyors, racks, etc. That's unusual, but something that someone in your type of business may be able to use.

The big problem is a common one that I've talked about over and over again: it's amazing that even the big CPA firms often do not have anyone who really knows sales and use taxes inside and out (at least handy to where you are). For example, the resident expert may not know that there's that one state that has that warehousing exemption!

So make sure you're talking to the top sales tax expert at the firm, regardless of their physical location. And make sure they look for any industry specific exemptions.

And, much as I hate to admit it, pay attention to the other potential taxes as well:

Income taxes (both corporate and personal - you'll have staff there)

Gross receipts taxes

Business occupation taxes

Employment taxes (your list mentioned California - beware!)

Property taxes

and other too-numerous-to-be-mentioned-here taxes

And many of these are administered at the county, city or district level, so it's not just about the state.

That's the best solution.

The cheap solution...

Pick your locations purely on operational grounds. Then buy a copy of the American Bar Association's Sales and Use Tax Deskbook. It's close to $300, but is the best single source of SUT laws that I've seen. You can get a pretty good idea of what's going on by using this book. Review the chapter for the state you're considering. If it looks too messy, then move on to the next state.

Another nice thing about this book is that it gives you the chapter authors for every state. Expensive, but well qualified people who can help you.

In other words, do your own research, but use a good tool to do the research.

Unfortunately, that doesn't help with the other taxes. And they can be nasty.

I think, in the long run, you'd be safer using the expensive approach - hire some pros. But make sure they actually are experts at sales and use taxes, dang it!

Sales Tax Guy

"We're a non-US company who has, up until now, avoided a physical presence in the US. We ship products to US customers (usually distributors and dealers) but have no reps, warehouses, plants, offices, etc. anywhere in the States. We're considering establishing warehouses in a few places and figure that will give us nexus in those states. Where do we find advice on making this decision that isn't going to be expensive?"

That last question makes this question pretty much applicable to all of you...

There really isn't a cheap solution. The best (and most expensive) one is to hire one of the giant CPA firms and have them do a study for you. It would take into consideration sales and use tax rates, complexity, audit friendliness, rules about nexus, certificate requirements, drop shipping, any possible and unusual exemptions you might be able to take, etc.

For example, there's at least one state that has an exemption for warehousing equipment, conveyors, racks, etc. That's unusual, but something that someone in your type of business may be able to use.

The big problem is a common one that I've talked about over and over again: it's amazing that even the big CPA firms often do not have anyone who really knows sales and use taxes inside and out (at least handy to where you are). For example, the resident expert may not know that there's that one state that has that warehousing exemption!

So make sure you're talking to the top sales tax expert at the firm, regardless of their physical location. And make sure they look for any industry specific exemptions.

And, much as I hate to admit it, pay attention to the other potential taxes as well:

Income taxes (both corporate and personal - you'll have staff there)

Gross receipts taxes

Business occupation taxes

Employment taxes (your list mentioned California - beware!)

Property taxes

and other too-numerous-to-be-mentioned-here taxes

And many of these are administered at the county, city or district level, so it's not just about the state.

That's the best solution.

The cheap solution...

Pick your locations purely on operational grounds. Then buy a copy of the American Bar Association's Sales and Use Tax Deskbook. It's close to $300, but is the best single source of SUT laws that I've seen. You can get a pretty good idea of what's going on by using this book. Review the chapter for the state you're considering. If it looks too messy, then move on to the next state.

Another nice thing about this book is that it gives you the chapter authors for every state. Expensive, but well qualified people who can help you.

In other words, do your own research, but use a good tool to do the research.

Unfortunately, that doesn't help with the other taxes. And they can be nasty.

I think, in the long run, you'd be safer using the expensive approach - hire some pros. But make sure they actually are experts at sales and use taxes, dang it!

Sales Tax Guy

| See disclaimer |

| Here's information on our upcoming seminars and webinars |

| And please don't forget to visit our advertisers! |

Wednesday, July 22, 2009

The Four Loopholes (Loophole Number 1)

There are four loopholes which created the need for use tax. Over a short period of time after inventing sales tax, the states started discovering that there were some situations where they weren't able to get the sales tax revenue they were expecting. We'll use this series of posts to discuss each one.

There are four loopholes which created the need for use tax. Over a short period of time after inventing sales tax, the states started discovering that there were some situations where they weren't able to get the sales tax revenue they were expecting. We'll use this series of posts to discuss each one.Purchases in another state

Say the rate where you are, in Vancouver, Washington is about 9%. But if you cross the bridge and go to a mall in Portland, Oregon (a 15 minute drive), you'll pay zero % sales tax. Where are you going to buy your big screen TV? Something tells me that, per capita, there are a lot fewer appliance stores in Vancouver than there are in Portland. Just a guess.

There's not a whole lot Washington can do about your buying that TV in Oregon. It's not like they can post border guards. You might leave a trail however. A woman in Washington bought a TV with a store account in Oregon, took the set home, and three months later, got a letter from Washington demanding the use tax.

She left a trail. The store filed a lien on the TV in Washington, where those records are computerized. So all the Washington revenuers have to do is scan the liens looking for one filed by an Oregon seller. Bingo. Revenue!

Pay cash though, and all that exists is the paperwork in the seller's offices. Unless they get audited..... Not that I'm suggesting this method of avoiding your proper Washington taxes, though. I'm just sayin'.

And I know of no state that routinely audits individuals for use tax. First of all, individuals don't keep sufficient records of all their purchases and receipts (except for the more anal among you). So there isn't anything to audit. Plus it's politically unwise to audit taxpayers (and voters) for a tax they didn't realize they owed. Most people who go to Oregon to buy their stuff don't know about use tax. They just think they're avoiding sales tax legitimately.

But if you're a business, oh, yeah. They'll find you. It's called "being audited."

The problem for the states is that they can't charge you sales tax since the sale occurred in another state and they can't reach that transaction. But they can impose use tax. You did, after all use that TV once you unloaded it in your driveway.

So if you buy something in one state where the rate is lower than the one where you will eventually use it, the state will impose use tax on your use of it in that state.

Use tax therefore plugs the loophole of your buying stuff in another state.

Sales Tax Guy

| See disclaimer |

| Here's information on our upcoming seminars and webinars |

| And please don't forget to visit our advertisers! |

| Picture note: the picture above is of the Columbia River, just east of Portland, Oregon and is hosted on Flickr. If you'd like to see a larger version, click here, then click on the "all sizes" button above the picture. |

Monday, July 20, 2009

Making sales you didn't know were taxable

Part of a continuing series

Part of a continuing seriesI had a guy in my seminar in state "A". He was an equipment rental company. He had stores in both state A and also the next-door state "B".

The tax rate in state A is about 9%. The tax rate in state B is about 6%. If you're renting a very expensive piece of equipment, you just might be thinking you'll rent it in state B, bring it back to state A and save yourself 3% sales tax on the rental.

Unfortunately, for the guy in my class, he didn't realize that the vast majority of the states require that you charge the sales tax on rental of tangible personal property (TPP) based on where it's used, not simply the location it is rented from.

So, this guy got audited by state A. And they nailed him. If I remember, the assessment was in the neighborhood of $500,000. That's half a million dollars, folks. For a really bad mistake.

Frankly, I'm surprised that someone in that business hadn't known about this rule. Could it possibly be because his CPA and lawyer didn't know what they didn't know and gave him bad advice? Or no advice at all? Nah.

So if you're in the rental business folks, watch where your equipment is being used.

By the way, you're probably asking how the rental company could have known where the equipment was being used. How could they have known to charge the tax for state A as opposed to the rate in state B where the store is? Because most of the time, the rental company delivered the equipment to the job site. Ahem.

Sales Tax Guy

| See disclaimer |

| Here's information on our upcoming seminars and webinars |

| And please don't forget to visit our advertisers! |

| Picture note: the illustration above is hosted on Flickr. If you'd like to see a larger version, click on the picture, then click on the "all sizes" button above the picture. |

Thursday, July 16, 2009

Tuesday, July 14, 2009

Opening Up the Can of Worms

So you decide that you need to register in another state. Believe it or not, there are a few reasons why you might want to do this:

So you decide that you need to register in another state. Believe it or not, there are a few reasons why you might want to do this:1. You actually have nexus in that state and you'd kind of like to obey the law. Right.

2. You have a big, gigantic customer who insists you collect taxes from him for your deliveries into another state.

3. You decide that registering in that state would be a good way of solving your Nutty Drop Ship Law problems.

4. You are dealing with a government agency in a state that requires you to be registered for sales and use taxes in order to bid on their business (more and more are doing this).

Well, be careful. You are opening up the proverbial can of worms.

There are several problems:.

1. You 'll be filing more returns. More work. More cost. Maybe you'll finally have to buy that sales tax software you've been getting the mailings about.

2. You'll attract the attention of the state you're registering in. Not only might an audit be imminent, but they will probably want to talk to you about all the other state taxes that you might owe, like income taxes, franchise taxes, occupation taxes, etc.

3. You'll lose a competitive advantage, depending on your market. If your customers buy from you, at least in part, because you're not charging them tax, then by registering, you'll lose some sales. Your sales and marketing people will hate you. They already hate you, it'll just be worse.

4. If you've been selling into the state for several years, you have an open liability going back all the way. Most states have no statute of limitations protection if you've never filed a sales and use tax return, which you obviously haven't. So beware!

I'm not saying you shouldn't register if you need to register. But recognize you're opening a can of worms and you need to get professional guidance.

Sales Tax Guy

| See disclaimer |

| Here's information on our upcoming seminars and webinars |

Picture note: Sorry, just clip art. I don't fish, so I just haven't had the opportunity to photograph a big, steaming can of worms. Maybe someday.

Friday, July 10, 2009

You can't just charge tax

I had an email from a reader the other day asking a follow-up question to the nutty drop ship rule article. [I just reread it and, other than the addition of a chart, it still works...dang I'm good. But I digress.]

Now you're going to have to go back and get the cast of characters straight in that article. The reader is Curly. She goes ahead and pays tax to the vendor (Larry). But she doesn't want her customer (Moe) to have to pay the tax later. So she asked if she can just show the tax on her invoice to Moe so he (and the auditor) can see that it has been paid.

Every state is different in this, so you must research this on your own. But here's the thing. You can't charge your customer sales or use tax unless you actually are registered in the state. This is the law in most states. There are a couple where this isn't the case, and many states have some sort of temporary permitting capability. But the point of this article, even though I'm roping in the drop ship issue, is unless you are registered in the state, in some way, for sales and use taxes, you cannot legally collect that state's tax.

So generally, Curly can't charge his customer tax. I would say that you have to be very careful about this. If you want to simply show the tax as a separate cost, built into the price of the goods, along with inbound freight, labor, expenses, materials costs, etc., that might be OK. The taxes you pay are a cost of doing business.

But if you have a "merchandise total" and then another number for tax, that's going to look fishy and might get you into trouble. It sure looks like you're charging them tax.

The other thing to remember is that the customer might question the charge. He'll be wondering why he has to pay tax. He thought, by buying from you, that he wouldn't have to worry about paying tax. Now you're charging him tax? The fact that the total at the bottom of the invoice is what you quoted probably isn't going to help. And it'll just confuse him more. Can your customer service people field these kinds of questions?

And if that weren't enough, the auditor probably isn't going to care about any "taxes" on the invoice unless you're registered to collect the tax in her state. So putting something called "tax" on the invoice isn't likely to help anyway.

Another option is to do what destination state (where Moe is) wants you to do - register. Then you'll be able to buy tax free because you'll have the proper resale certificate, and you'll be able to legitimately charge your customer tax giving him a proper receipt for taxes paid. But that opens up another can of worms.

I've given you a lot of generalities in this article. You must check to see what the rules are in the destination state.

Sales Tax Guy

Now you're going to have to go back and get the cast of characters straight in that article. The reader is Curly. She goes ahead and pays tax to the vendor (Larry). But she doesn't want her customer (Moe) to have to pay the tax later. So she asked if she can just show the tax on her invoice to Moe so he (and the auditor) can see that it has been paid.

Every state is different in this, so you must research this on your own. But here's the thing. You can't charge your customer sales or use tax unless you actually are registered in the state. This is the law in most states. There are a couple where this isn't the case, and many states have some sort of temporary permitting capability. But the point of this article, even though I'm roping in the drop ship issue, is unless you are registered in the state, in some way, for sales and use taxes, you cannot legally collect that state's tax.

So generally, Curly can't charge his customer tax. I would say that you have to be very careful about this. If you want to simply show the tax as a separate cost, built into the price of the goods, along with inbound freight, labor, expenses, materials costs, etc., that might be OK. The taxes you pay are a cost of doing business.

But if you have a "merchandise total" and then another number for tax, that's going to look fishy and might get you into trouble. It sure looks like you're charging them tax.

The other thing to remember is that the customer might question the charge. He'll be wondering why he has to pay tax. He thought, by buying from you, that he wouldn't have to worry about paying tax. Now you're charging him tax? The fact that the total at the bottom of the invoice is what you quoted probably isn't going to help. And it'll just confuse him more. Can your customer service people field these kinds of questions?

And if that weren't enough, the auditor probably isn't going to care about any "taxes" on the invoice unless you're registered to collect the tax in her state. So putting something called "tax" on the invoice isn't likely to help anyway.

Another option is to do what destination state (where Moe is) wants you to do - register. Then you'll be able to buy tax free because you'll have the proper resale certificate, and you'll be able to legitimately charge your customer tax giving him a proper receipt for taxes paid. But that opens up another can of worms.

I've given you a lot of generalities in this article. You must check to see what the rules are in the destination state.

Sales Tax Guy

| See disclaimer |

| Here's information on our upcoming seminars and webinars |

Wednesday, July 08, 2009

Golden Rule: The Basis of Tax

This is one of a series on how to handle items that affect the "basis" of tax.

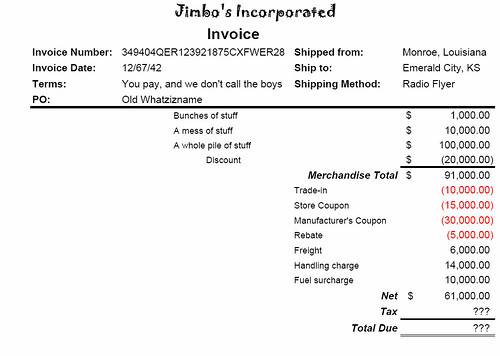

Once we have determined that a sale is taxable, there remains another problem. We are going to add sales or use tax of, say, 7%. But 7 % of WHAT?

The invoice above is taxable because stuff is always taxable (that joke sounds better when I do it in the seminar - trust me). So obviously the 7% is going to be applied to the merchandise total of $91,000. But what are we going to do with those extra things, like coupons, rebates, freight charges, etc.

The rule is generally known as basis of tax - what we are going to take 7% of. Basis of tax deals with the extra items on an invoice, that is already taxable, and whether those items will be added to the basis or subtracted from the basis. So here's the actual golden rule:

All of the charges on a taxable invoice will be added to the tax basis and are therefore taxable. But all of the deductions from a taxable invoice will NOT reduce the tax basis...they have no effect on the tax.

This sounds unfair. But when you start taking apart these rules in each state, you'll find there are LOTS of exceptions. But it's helpful to start with the assumption that any charges will be added to the taxes. But deductions do not reduce the taxes.

Also, remember - this rule is only relevant if the sale is taxable. If the sale (or purchase) wasn't taxable, then forget about it. Move along, nothing to see here. We don't care about those extra items...there is no basis of tax if there isn't a tax in the first place..

For example: If I'm charging a customer freight for a shipment of no-charge parts that are covered by a warranty, then the sale isn't taxable. And the freight charge won't be taxable either. If there is no taxable sale, there's no tax. And there won't be any basis. So you're finished.

That's the theory, anyway. I have seen some weird spins on these rules, so it's important to check the applicable state's rules to make sure you're not missing anything. For example, some states will say that installation charges are taxable, regardless of the taxability of the sale of the stuff being installed. Go figure.

Sales Tax Guy

We have more articles on the basis of tax.

Picture note: the illustration above is hosted on Flickr. If you'd like to see a larger version, click on the picture or the Flick link, then click on the "all sizes" button above the picture.

.

Once we have determined that a sale is taxable, there remains another problem. We are going to add sales or use tax of, say, 7%. But 7 % of WHAT?

The invoice above is taxable because stuff is always taxable (that joke sounds better when I do it in the seminar - trust me). So obviously the 7% is going to be applied to the merchandise total of $91,000. But what are we going to do with those extra things, like coupons, rebates, freight charges, etc.

The rule is generally known as basis of tax - what we are going to take 7% of. Basis of tax deals with the extra items on an invoice, that is already taxable, and whether those items will be added to the basis or subtracted from the basis. So here's the actual golden rule:

All of the charges on a taxable invoice will be added to the tax basis and are therefore taxable. But all of the deductions from a taxable invoice will NOT reduce the tax basis...they have no effect on the tax.

This sounds unfair. But when you start taking apart these rules in each state, you'll find there are LOTS of exceptions. But it's helpful to start with the assumption that any charges will be added to the taxes. But deductions do not reduce the taxes.

Also, remember - this rule is only relevant if the sale is taxable. If the sale (or purchase) wasn't taxable, then forget about it. Move along, nothing to see here. We don't care about those extra items...there is no basis of tax if there isn't a tax in the first place..

For example: If I'm charging a customer freight for a shipment of no-charge parts that are covered by a warranty, then the sale isn't taxable. And the freight charge won't be taxable either. If there is no taxable sale, there's no tax. And there won't be any basis. So you're finished.

That's the theory, anyway. I have seen some weird spins on these rules, so it's important to check the applicable state's rules to make sure you're not missing anything. For example, some states will say that installation charges are taxable, regardless of the taxability of the sale of the stuff being installed. Go figure.

Sales Tax Guy

| See disclaimer |

We have more articles on the basis of tax.

| Here's information on our upcoming seminars and webinars |

| And please don't forget to visit our advertisers! |

Picture note: the illustration above is hosted on Flickr. If you'd like to see a larger version, click on the picture or the Flick link, then click on the "all sizes" button above the picture.

.

Monday, July 06, 2009

What state are you asking about?

This should be the first question out of anyone's mouth when asked a sales and use tax question. If you call your accountant or lawyer, and they just give you an answer, without asking that Question, they have missed three of the most fundamental rules of SUT, the Golden Rules.

This should be the first question out of anyone's mouth when asked a sales and use tax question. If you call your accountant or lawyer, and they just give you an answer, without asking that Question, they have missed three of the most fundamental rules of SUT, the Golden Rules.They may not realize that the delivery state makes the rules - that is the state that has jurisdiction. So the answer must be based on that remote state, not the ship-from state. But since your professional hasn't even asked the Question, he or she doesn't know about the remote state.

And they may not understand that every state has different rules. What's taxable in your state won't be taxable in the other state. And what's exempt there, won't be exempt where you are. There might be completely different rules in that other state, but your professional doesn't even know that there is another state involved.

So can you see that your chosen SUT professional has really messed up if he or she doesn't ask, "What state are you asking about?"

There is an exception to this. If you have a business that never ships your product out of state, you never perform services in or visit another state for business purposes, and your professional knows this from previous experience with you, then not asking the Question is OK. But does that professional really know? Either about your business, or about the golden rules of sales and use taxes?

If they don't ask the Question, be afraid. Be very afraid.

Sales Tax Guy

| Here's information on our upcoming seminars and webinars |

| And please don't forget to visit our advertisers! |

Picture note: It's a picture of me. I figure it's safer to use my picture when I'm mocking. Less lawsuits that way.

.

Thursday, July 02, 2009

Private Letter Rulings

If you are stumped and there isn't a rule, bulletin, regulation, law, court case, or interpretation that addresses your particular question, you've looked in all the places we've talked about here, and you can't get anyone to give you an authoritative answer, there may be help.

Most states will give you a private letter ruling, opinion letter, or something similarly named. The idea is that you formally ask the revenue department about your situation and they give you a formal, take-it-to-the-bank answer. It's not a guess, it is, for you, the answer. And they have to honor it when you get audited, assuming you didn't fib when you gave them the information, and things haven't changed.

Sometimes these letters are published so that others can find some guidance if they're in similar situations to yours.

Yay! Why didn't we do this before???

Because, to do it right, it is expensive. You want to do this anonymously so that the state doesn't know who you are, and send auditors out in the night to ambush you. You want to go through an attorney or CPA. They'll ask the question, keeping your name out of the discussion. In addition, if the professional specializes in sales and use taxes, they might even be able to answer the question without having to get an opinion letter.

This ain't gonna cost you a couple of hundred bucks. This will probably cost a couple of thousand. But if you're looking at a big issue, involving lots of money and risk, this is a very good way of getting a good, reliable answer.

Sales Tax Guy

Most states will give you a private letter ruling, opinion letter, or something similarly named. The idea is that you formally ask the revenue department about your situation and they give you a formal, take-it-to-the-bank answer. It's not a guess, it is, for you, the answer. And they have to honor it when you get audited, assuming you didn't fib when you gave them the information, and things haven't changed.

Sometimes these letters are published so that others can find some guidance if they're in similar situations to yours.

Yay! Why didn't we do this before???

Because, to do it right, it is expensive. You want to do this anonymously so that the state doesn't know who you are, and send auditors out in the night to ambush you. You want to go through an attorney or CPA. They'll ask the question, keeping your name out of the discussion. In addition, if the professional specializes in sales and use taxes, they might even be able to answer the question without having to get an opinion letter.

This ain't gonna cost you a couple of hundred bucks. This will probably cost a couple of thousand. But if you're looking at a big issue, involving lots of money and risk, this is a very good way of getting a good, reliable answer.

Sales Tax Guy

| Here's information on our upcoming seminars and webinars |

| And please don't forget to visit our advertisers! |

Subscribe to:

Posts (Atom)