Bill* invented a machine to curry wockies.* His problem was that while he knew the machine would be a real boon to the wocky service industry, it was really, really expensive. He had a lot of trouble convincing the industry to use his machine because of the ridiculously high initial cost. Finally, one of his investors suggested a tactic that has been long used by inventors with money. He bought his customers and made them use the Frazier Wocky Currier*.

Bill* invented a machine to curry wockies.* His problem was that while he knew the machine would be a real boon to the wocky service industry, it was really, really expensive. He had a lot of trouble convincing the industry to use his machine because of the ridiculously high initial cost. Finally, one of his investors suggested a tactic that has been long used by inventors with money. He bought his customers and made them use the Frazier Wocky Currier*.In the Great State of East Dakota*, which is in the heart of the wocky region of the country, he bought ten small little wocky service companies, spread throughout the state. Since he didn’t really want to get into the wocky service business, the typical deal was, “Here’s a pile of money for your company. You keep running it the way you like. You can even keep the same name on the sign. I don’t care. But, whenever a situation comes up where you need to curry wockies, you have to use my machine.”

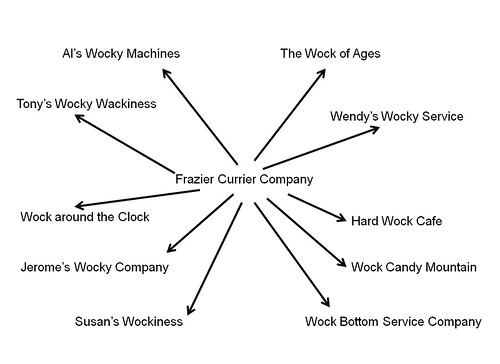

From a financial perspective, he simply bought all of the shares in the corporations of these little service companies and let them stand as separate, but commonly owned, subsidiaries of his own company, The Frazier Currier Company*.

His corporate empire looked something like this*

The machine was a success. It was incredibly effective and the customers were thrilled. In fact, the local companies actively looked for opportunities to curry wockies, so they could use the machines even more. Everyone made money.

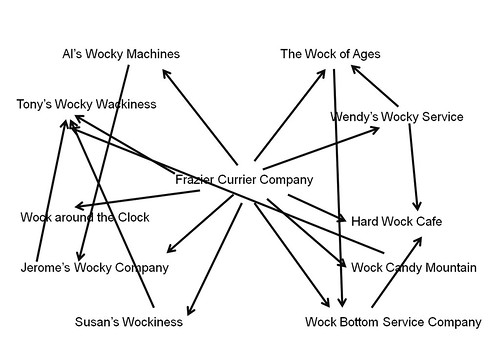

The Frazier Currier Company manufactured the machines and then shipped them to the service companies.

Business got so good that sometimes they couldn’t get enough machines. So they would move machines from one service company to another to meet local demand.

Then the State of East Dakota audited them.

And the auditor noticed that they were selling these very expensive machines from the parent to the subsidiaries and no sales tax was being charged. And that the subsidiaries were selling the machines to each other, and no sales tax was charged.

Frazier Currier Company argued that these were just movements of machines between branch locations, that they weren’t sales.

But the auditor pointed out that every branch, as well as the parent, was a separate corporation. And in East Dakota (and in most states), corporations are legal persons. Transfers of tangible personal property and taxable services between persons, are sales. Period. The assessment was over $10,000,000.

The only way the Frazier Currier Company was able to negotiate the assessment down, was by bringing East Dakota’s leading bankruptcy attorney to the negotiations.

So what’s the moral of the story here?

First of all, bring a bankruptcy attorney to the negotiations.

Seriously, you need to make sure, when you are transferring taxable goods and services among subsidiaries and parents, that you are properly taxing the transactions. In most states, they look at the form and nature of the transaction. Is there formal paperwork? That makes it look more like a sale. Is there just a note to the bookkeeper so he knows where the machine is? Maybe it’s not a big deal. Is it an occasional sale? That might get you off the hook. But you need to know.

And here’s the kicker. This is not well documented in most state’s statutes and regulations. This is one of those areas where you need a local consultant who knows the customs and audit practices of East Dakota or whatever state you're in.

The irony is that, of all of the accountants and lawyers that Bill used when he set up the business, he didn’t have a sales tax expert. That august personage could have told Bill to set up leasing arrangements so that every machine is owned by The Frazier Currying Company and is LEASED to the subsidiaries. Because, in East Dakota, there’s an exemption to the rule for intercorporate transactions if they're leases.

*I’m using fake names to either protect the innocent, the guilty or to just be funny.

The Sales Tax Guy

http://salestaxguy.blogspot.com

See the disclaimer - this is for education only. Research these issues thoroughly before making decisions. Remember: there are details we haven't discussed, and every state is different. Here's more information

Get these articles in your inbox - subscribe at http://salestaxguy.blogspot.com

Don't forget our upcoming seminars and webinars.

http://www.salestax-usetax.com/

Picture note: the image above is hosted on Flickr. If you'd like to see more, click on the photo.

No comments:

Post a Comment